Several investment companies have made a name for themselves in recent years through high-yield income-oriented funds like YieldMax, NEOS, and Defiance.

The number of high-income funds being launched has grown significantly to the point that it has become overwhelming for me to cover them all and pick out the best few.

I often wondered what it would be like if one were to buy all the high-yield funds without thinking.

Of course, YouTube read my mind and slid a small YouTube channel featuring an American expat’s high-yield ETF portfolio in front of me.

This YouTuber is The Dividend Nomad. He’s a 42-year-old American expat living in China for 14 years and running a high-yield investing experiment.

The goal of his portfolio is to generate enough income to help him retire in foreign countries where his work opportunities are minimal.

With just $22k, he has collected about $670 this month, yielding approximately 36%.

Impressive, but at what cost?

Today, we’ll examine his portfolio, how he generates these massive yields, and whether you should do the same.

A Collection of Ultra-High-Yielding ETFs (Everything Yields 10%+)

The Digital Nomad’s portfolio consists of the following 12 holdings and the approximate percentage of the portfolio each holding occupies:

- QYLD — Global X NASDAQ 100 Covered Call ETF | 0.08%

- SPYI — Neos S&P 500(R) High Income ETF | 4.90%

- SPYT — Defiance S&P 500 Target Income ETF | 3.55%

- QQQI — NEOS NASDAQ-100(R) High Income ETF | 4.53%

- QQQY — Defiance Nasdaq 100 Enhanced Options Income ETF | 23.32%

- IWMY — Defiance R2000 Enhanced Options Income ETF | 8.22%

- JEPY — Defiance S&P 500 Enhanced Options Income ETF | 11.68%

- KLIP — Kraneshares China Internet And Covered Call Strategy ETF | 6.28%

- FEPI — REX FANG & Innovation Equity Premium Income ETF | 5.34%

- SVOL — Simplify Volatility Premium ETF | 1.74%

- TSLY — YieldMax TSLA Option Income Strategy ETF | 18.12%

- YMAX — YieldMax Universe Fund of Option Income ETFs | 3.20%

All funds on this list employ some sort of options and derivative strategy to generate their massive yields. No ETF on this list has a current yield of less than 10% either, with many yielding above 20% and some close to triple-digits.

Let’s take a closer look at some of the individual holdings.

Defiance’s 0DTE Cash-Secured Put Funds

First, let’s look at Defiance’s 0DTE funds that sell cash-secured puts. These funds are QQQY, JEPY, and IWMY and comprise The Dividend Nomad’s most significant holdings.

With such a big focus on yield, it’s easy to see why these three funds are so appealing.

QQQY, JEPY, and IWMY have yields of 66.36%, 54.28%, and 102.97%, respectively. Imagine getting more in dividends than what your portfolio is worth.

Of course, these massive yields come at a cost. As discussed in a recent article about these funds, all three funds have suffered significant and rapid NAV depletion, which I’m not a big fan of.

QQQY and JEPY, Where Are They Now? (66.36% and 54.28% Yields)

More time will tell if these funds are worth investing in, but the idea of my principal eventually going to zero doesn’t sit well with me.

YieldMax’s Synthetic Covered Call Strategies

The following largest holdings are in YieldMax funds, consisting of approximately 21% when you add his TSLY and YMAX funds together.

These are also ultra-high-yielding funds with current respective yields of 58.05% and 37.37%.

YieldMax has become famous for its synthetic covered call funds, which sell covered calls on individual stocks instead of indexes. The idea is that these individual stocks have higher volatility, which increases the option premium and, hence, the dividend payouts.

TSLY is the fund where YieldMax uses this covered call strategy on Tesla stock (TSLA), and I covered it back in June 2023.

Beware Of TSLY And Its 57.81% Dividend Yield — It Just Doesn’t Make Sense

The popularity of TSLY prompted YieldMax to launch more funds on different stocks, and ultimately, they created a fund of funds — YMAX — to hold each one in equal weight.

Personally, I would sell the entire TSLY holding and shift the funds into YMAX. I know The Digital Nomad is currently holding on to a loss with TSLY (even including the dividends), but there’s no reason to hold both YMAX and TSLY unless you want a higher exposure to Tesla.

More and More Call Options

Next, we have all the other ETFs that generate most of their dividend payments through selling call options.

These funds are QYLD, SPYI, SPYT, QQQI, KLIP, and FEPI.

Most of these funds are simple. They hold assets and then sell calls on them to generate option premiums. The exception is SPYT, which sells call spreads instead—a strategy where one sells a call and buys a call further out of the money as a safety net.

For more information on covered calls and how funds use them to pay out double-digit yields, check out this article:

An Introduction To Covered Calls And How Ultra High Yield Funds Achieve 10%+ Yields

To me, these holdings are too redundant.

I would not buy both QYLD and QQQI. Both are essentially exposure to the NASDAQ 100 plus call options. The same goes for SPYT and SPYI, which are the same but on the S&P 500.

You don’t need FEPI either when you have so much exposure to the NASDAQ 100 and the YieldMax funds.

Yes, the funds have enough differences to warrant investments in multiple ones, but there’s no clear strategy here.

If you’re buying QYLD, what about XYLD and RYLD? Why not JEPI and JEPQ?

When buying so many different funds, there’s an illusion of diversification. While it might seem like you’re protecting yourself, all of these funds are tied to stocks, particularly the U.S. stock market.

If the U.S. stock market crashes, all these funds go down with it regardless of their difference in strategies. The difference is that some will crash harder, and others will crash less.

KLIP is the only actual form of diversification (along with SVOL, which we’ll discuss next) by investing in China’s stock market.

If it were me, I would eliminate QYLD, SPYT, and FEPI and add TLTW, LQDW, and HYGW for bond exposure and massive yields.

A Futures ETF To Round Things Out

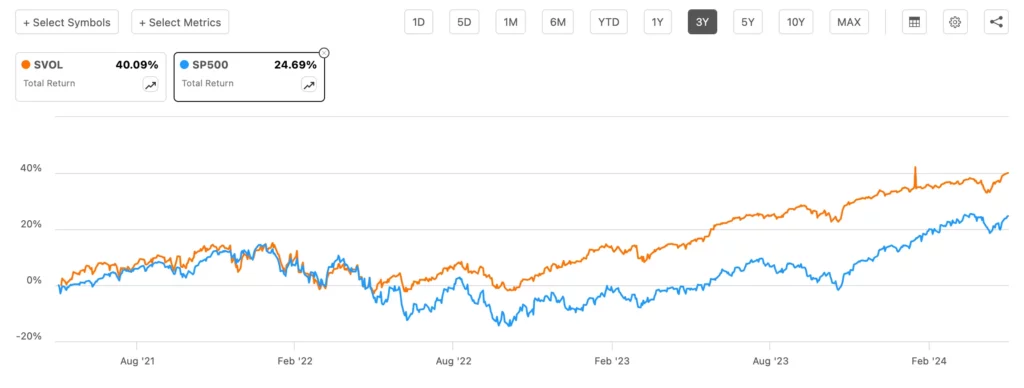

For the final piece of this portfolio, we have SVOL. This fund has been the most impressive, outperforming the S&P 500 in the last three years while maintaining above 15% yields.

SVOL differs from the other funds in that it uses VIX futures. It generates most of its premiums by shorting the VIX.

For a more in-depth explanation, see this article:

SVOL Currently Yields 17.68%; Is This Dividend Sustainable?

The benefit of SVOL is you’re getting away from relying on call options to generate income, as SVOL thrives from periods of lower volatility versus the increased option premiums you gain from higher volatility markets with call options.

If I were The Dividend Nomad, I would increase my SVOL position to 5–10% of the portfolio.

Always Ask If Income Is Really Your Goal

As you may have already inferred, the cost of this 36% yield is NAV depletion. The Dividend Nomad currently has an unrealized loss of about $3k though the dividends have made him profitable.

In terms of total return, an investment into the S&P 500 will likely outperform this portfolio in the long run, so you need to consider whether income is your goal.

Yes, 36% yearly dividends paid monthly sounds incredible, but you could also do the same by selling shares as needed.

These dividends are also heavily taxed if you’re not investing in a tax-sheltered account, which will drastically reduce your gains if your taxes are high.

As discussed in an article about why I’m investing in income as a 21-year-old, consider your opportunity cost.

Why I’m Investing in This Two-Fund Portfolio Yielding 11.34% in My 20s

Is what I gain from the income worth the gains I miss out on higher-returning investments?

One such investment could be an investment in yourself.

Instead of investing thousands of dollars for a couple of hundred dollars in dividends every month, what if you can build a cash flow machine with the same results for a fraction of the cost?

Find out how in this FREE training by clicking here.

Do you love these investing portfolio articles? All portfolio articles have been saved to the list below, which you can access at your convenience.

Investment Portfolio Articles

Financial Disclaimer: The views in this article are the author’s personal views. This commentary is provided for general informational purposes only. It does not constitute financial, investment, tax, legal, or accounting advice, nor does it constitute an offer or solicitation to buy or sell any securities referred to. Individual circumstances and current events are critical to sound investment planning; anyone wishing to act on this article should consult with their advisor. The information provided in this article has been obtained from sources believed to be reliable and is believed to be accurate at the time of publishing, but we do not represent that it is accurate or complete, and it should not be relied upon as such. Investing in stocks, bonds, exchange-traded funds, mutual funds, and money market funds involves the risk of loss. Their values change frequently, and past performance may not be repeated.

Affiliate Link Disclosure: You may assume all links in this article are affiliate links. If you purchase any product or service through the link, I may be compensated at no extra cost to you.

Visit us at DataDrivenInvestor.com

Subscribe to DDIntel here.

Featured Article:

Singapore: Unveiling a Tapestry of Possibilities and Global Connections

Introducing Singapore’s Fund Platform | Accelerating Fund’s Setup, Launch, and Operational Efficiency

Join our creator ecosystem here.

DDI Official Telegram Channel: https://t.me/+tafUp6ecEys4YjQ1

Follow us on LinkedIn, Twitter, YouTube, and Facebook.

Originally published on Medium.com. Get a Medium membership and read articles like this one ad-free.

Leave a Reply